This post was originally published on this site

Overview

We maintain our bullish view on Pluralsight (NASDAQ:PS), the leading cloud-based solution for technical skills development. The share price has appreciated by over 40% since last September when we covered the stock for the first time. Back then, we had our share of doubts about the management’s execution. However, the consistent outperformance in the next few months that followed proved us wrong. The execution has been solid as of Q1, and therefore, we continue to believe in the management’s ability to convert the temporary tailwinds the business currently sees, into long-term opportunities.

Catalyst

As many of the similar online education businesses have received a tailwind during the COVID-19 outbreak, so has Pluralsight. In Q1, the company beat its guidance as revenue grew by ~33%. From a macro standpoint, the increasing work-from-home and stay-at-home trend has a been near-term catalyst. On the other hand, the solid execution will maintain a very favorable outlook for the business.

(Source: pluralsight.com)

Having covered the company twice last year, we remain confident in the demand for the offering and the management’s execution ability. Pluralsight still struggled with some sales execution issues last September, though the strong turnaround which involved an appointment of the new CRO turned us into a believer in the business.

The Free April campaign in Q1, for instance, was a very strategic move to drive word-of-mouth marketing on the B2C side, long-term B2B lead generation, and overall marketing cost saving. In Q1, it took only 10% -15% of the past marketing spending to execute the campaign and generate the kind of user traction it achieved during the Free April. Furthermore, as over 200,000 of the sign-ups were done with business emails, there is a clear opportunity to turn some of these B2C leads to long-term B2B deals as well.

(Source: company’s 10-K)

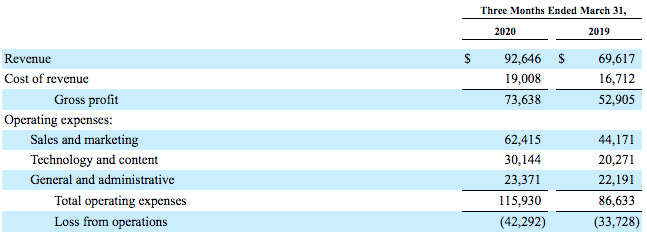

The strong execution in Q1 will also drive growth and margin expansion going forward. Gross margin has expanded by ~400bps as revenue grew by 33% YoY in Q1. Moreover, while the Free April campaign mostly targeted the B2C segment, the overall Q1 growth was primarily driven by the ~39% increase in B2B revenue. Therefore, we see an upside growth potential here as the business is yet to recognize the ROI from the Free April investments, which slightly widened the operating loss in Q1. In the meantime, the company has also done its best to maintain growth and save costs. In Q1, the company froze new hiring while also seamlessly shifting its ILT program to the cloud, which we believe was the major driver for the continuing strength in the B2B revenue and the net retention.

Risk

The company’s $550 million of cash and investments will give the company flexibility in terms of pursuing future growth opportunities. However, we believe that any new M&A deals may be out of the question, considering the potentially higher premium on the online education market today relative to pre-COVID-19. In the past, the company regularly leveraged strategic acquisitions to quickly scale the business by expanding its content library or features. In particular, we rated the company’s ~$60 million GitPrime acquisition highly, which becomes the Flow offering today.

Valuation

Most of the online education stocks, typically those with sizable B2C businesses, have been performing well during the pandemic, though the overall uncertainty remains. Indeed, except for Pluralsight and Chegg (CHGG), which drives over 90% of its revenue from students’ subscriptions of its homework help platform, all the other stocks in the peer group have not been as outperforming since the major sell-off in March.

(CHGG vs PS vs CSOD vs TWOU. source: stockrow)

In general, as we discussed, the P/S for these online education stocks have experienced some upticks in recent times despite the concern on the content delivery and sales execution, given the mix of offline/online approach inherent in their B2B business models and go-to-market. Most of the stocks in the group have a solid ~30% growth rate, except for Cornerstone (NASDAQ:CSOD), a B2B company developing an LMS (Learning Management System) that faced some headwinds in landing new clients in Q1. As Pluralsight successfully made a major adjustment by shifting its entire offline ILT program online, we may potentially see a further uptick on its P/S.

Upon the adjustment in Q1, growth remained solid at +30% while the 81% gross margin reflected a significant expansion from the prior year. 2U (TWOU) also made a similar adjustment, though we think it is fairly priced at ~3.3x P/S, considering its substantial inorganic growth. On the other hand, we believe that Pluralsight’s 6.7x P/S today is more attractive. Moreover, the current valuation was very similar to the ~6x P/S in September last year, when the company was facing an execution issue and without a CRO.

Disclosure: I am/we are long PS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.