This post was originally published on this site

Despite their fortress balance sheets and stress tests, U.S.’s banks have been weakened this year as inflation and the prospects of a recession weigh on the mightiest on Wall Street.

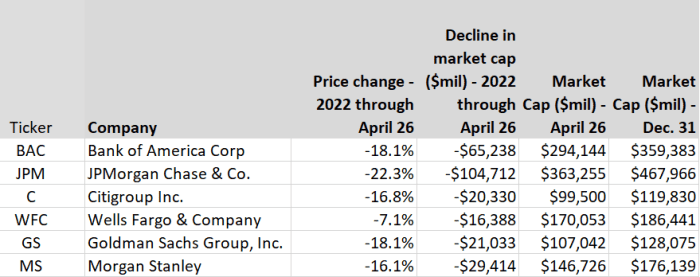

Investors have flashed a big red light at the six largest publicly traded U.S. banks, which have underperformed the broad market and erased a whopping $257 billion out of their combined $1.44 trillion market cap at the start of the year. (See chart).

MarketWatch/Philip van Doorn

The massive wealth evaporation has encompassed Dow Jones Industrial Average

DJIA,

components Goldman Sachs Group Inc.

GS,

(down 18.1% year-to-date) and JPMorgan Chase & Co.

JPM,

(down 22.3%). Other members of the ailing stock megaclub include Wells Fargo & Co. (down 7.1%), Bank of America (down 18.1%), Citigroup

C,

(down 16.8%) and Morgan Stanley

MS,

(down 16.1%).

Except for Wells Fargo, the group’s performance is worse than the 8.4% percent year-to-date loss of the Dow 30 and the 12.2% loss by the S& P 500

SPX,

In the broader banking and financial sector, the Financial Select Sector SPDR ETF

XLF,

is down 9.6% and the KBW Nasdaq Bank Index

BKX,

is off about 15%.

With headwinds from the Ukraine war, inflation on the rise, market volatility and the Fed poised to raise interest rates, capital markets have seized up, at least in terms of initial public offerings and other deal-making.

With their investment banking activities down and their capital ratios impacted by price drops in the Treasury market, bank earnings moved lower in the first quarter against a bumper crop of deal-making and recovery in the first quarter of 2021.

See: Goldman Sachs, Morgan Stanley, Citigroup report lower earnings

Ellen Hazen, chief market strategist and portfolio manager at F.L. Putnam Investment Management Co., said the bank’s thinner capital ratios have weighed on stocks because they raise the fear that credit quality could deteriorate in a recession.

“The conventional wisdom was that bank stocks would benefit from a steeper yield curve,” Hazen said. “Although the curve has gotten steeper, it hasn’t helped bank stocks. That’s because of concerns over an economic slowdown. This reflects the worry that the Fed may overshoot and in its desire to definitively quash inflation, and it will tip the economy into a recession.”

The current environment marks a sharp reversal from 2021 when bank stocks rallied on expectations that higher interest rates would boost net interest income.

However as 2022 got under way, inflation worsened with the Ukraine war and other factors.

The Fed’s expected interest rate hikes continue to create jitters around a drop in economic activity impacting banks.

This worry has outweighed any expected boost in net interest income that may come about as interest rates rise.

Also Read: The ‘Fed put’ is gone for now, top Wall Street strategist says

Moreover, as banks channel more capital to keep their capital ratios in line with regulatory requirements, they may trim the share buybacks that have been supporting growth in earnings per share.

Investors have seized on the tradition of a recession taking place 12 to 18 months after the yield curve between the three-year and 10-year Treasurys became inverted earlier this year.

Deutsche Bank analyst Matt O’Connor said in a Wednesday research note that bank stocks appear to be pricing in about a 50% chance of a recession. As of yesterday’s trades, bank stocks have fallen 21%, compared to a 30% drop on average during 27 bear markets since 1966.

In the severe COVID-19 stock selloff of March 2020, bank stocks fell 51%, by comparison.

O’Connor said Deutsche Bank remains positive on bank stocks, and lifted his 2022 earnings per share estimates by 6% on average.

“Markets are increasingly worried a recession or material slow down is

coming to the U.S. economy…yet loan growth is accelerating and there’s no

sign of banks tightening underwriting standards,” he said.

Among the megabanks, Wells Fargo

WFC,

and Bank of America

BAC,

remain his top picks. He noted that Bank of America signaled that it expects second-quarter net interest income to rise by $650 million over the first quarter, with sequential growth expected in the second half of the year.

Wells Fargo expects its fiscal 2022 net interest income to rise in the mid-teens from 2021’s level from loan growth and higher than expected rate increases. Wells Fargo also forecasts loan growth in the mid single digits in the fourth quarter.

Putnam’s Hazen remains bullish on Bank of America on expectations of greater net interest income, benign credit metrics and margin growth on its net interest income. The bank also has wide exposure to the U.S. consumer which has grown collective deposit balances by 40% since pre-COVID-19.

“Consumers are in a very strong space,” Hazen said.

— Philip van Doorn contributed to this report

Also Read: Economy shrinks 1.4% in first quarter, GDP shows, but mainly due to record U.S. trade deficit