This post was originally published on this site

European stocks were headed for their best week since March, and the fourth straight weekly gain on Friday, but will that positive momentum hold up with some of the biggest companies set to report next week, such as Ericsson, Royal Philips and Nestlé?

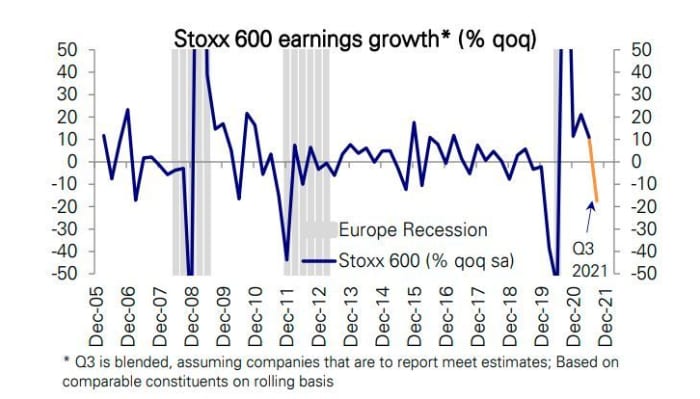

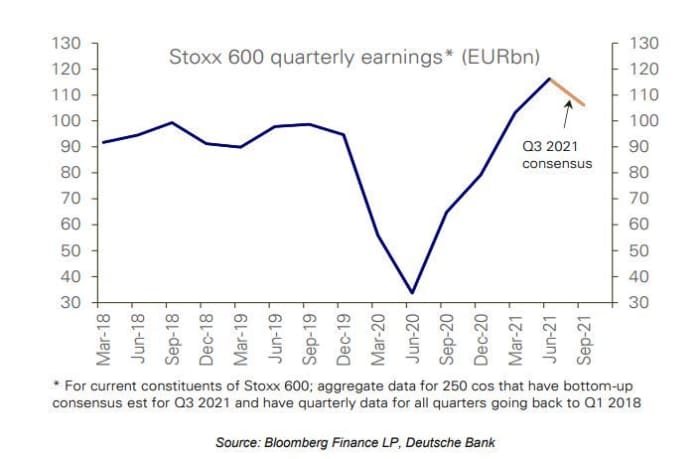

Deutsche Bank strategists believe the “enormous beats for the last five quarters,” similar to what was seen in the U.S. and elsewhere are likely to normalize in the third quarter. Consensus estimates project an 18% seasonally adjusted drop in earnings for Stoxx 600 companies, said a team led by Binky Chadha, in a note to clients.

The third quarter could mark the most negative reporting period outside of recessions for the Stoxx 600, they added.

“The decline is partly driven by the slowing in macro growth overall, but

also due to idiosyncratic factors affecting the financials and autos sectors. Excluding these, earnings are projected to continue rising. Much as in the U.S., we see earnings beating again but more modestly so than over the last few quarters,” said Chadha and the team.

Since last November, stocks in Europe have gained in lockstep with Wall Street. Deutche Bank notes that European forward price/earnings valuations are back to pre-pandemic levels, but at an extreme discount to the U.S. Much of that gap, though, is explained via the bigger role of megacap growth companies in the U.S., which have seen a rerating.

The big drag for Europe’s third quarter is expected to come from autos and financials, sectors that are geared toward economic recoveries, but with autos also taking hits from global supply shortages. Stripping out financials and autos, Stoxx 600 earnings should rise about 7.7% on the quarter, said Deutsche Bank.

Bank of America earlier this month cut its forecast for European equities, warning of a 10% drop by the end of the year amid fading economic growth momentum ahead for the region.

Barclays

BARC,

will help kick off earnings for financials next week, but the sector’s results will get under way in earnest the following week. The Stoxx Europe Banks

SX7P,

sector has rallied 37% this year, outstripping a 17% gain for the main index.

As for autos, data on Friday showed new-car registrations in the European Union slid 23% annually in September, dogged by a continuing lack of microchips that has dogged the global industry. Renault

RNO,

will be among the first auto names to report next Friday.

Renault was recently upgraded to buy from neutral at Bank of America, which noted some big model launches coming in 2022 and 2023, and analysts are upbeat on its cash flow prospects. As for the sector as a whole, a troubled third quarter with chip shortages is likely already priced in, they say, adding that investors should focus on the fourth-quarter outlook and guidance.

Among the biggest names reporting next week, investors will hear Philips

PHG,

PHIA,

report Monday, along with mining giant BHP Group

BHP,

BHP,

followed by from Swedish multinational networking and telecommunications company Ericsson

ERIC,

on Tuesday, along with food group Danone

BN,

and luxury goods group Kering

KER,

Wednesday will see tech giant ASML Holding

ASML,

report, along with food group Nestlé

NESN,

NSRGY,

and fertilizer company Yara International

YAR,

to name a few. Thursday’s batch includes miner Anglo American

AAL,

German software giant SAP

SAP,

SAP,

which pre-reported upbeat results earlier this week, Hermès International

RMS,

Barclays

BCS,

BARC,

and drinks maker Pernod Ricard

RI,

followed by rival Remy Cointreau

RCO,

on Friday and Renault.

The Stoxx Europe 600 index

SXXP,

rose 0.4% to 488 on Friday, a gain of nearly 3% for the week, which if holds, will mark the best weekly return since a 3.5% gain the week ended March 12. Banks were leading the gains, led by oil companies as energy prices climbed.

Hugo Boss

BOSS,

was a top performer, surging 4% after the German luxury fashion group lifted 2021 targets as its third-quarter sales and earnings exceeded pre-pandemic levels and market expectations