This post was originally published on this site

Mario Draghi famously likened the euro to a bumblebee; Morgan Stanley analysts say a record-breaking global stock-market rally reminds them of a duck: “calm above the surface, but furious churning below.”

The calm is reflected in a continued drop in realized, or actual, stock-market volatility. The analysts, led by Andrew Sheets, observed in a Friday note that realized, one-month equity volatility across the U.S., Europe and emerging markets has fallen to the 25th percentile of the last 15 years.

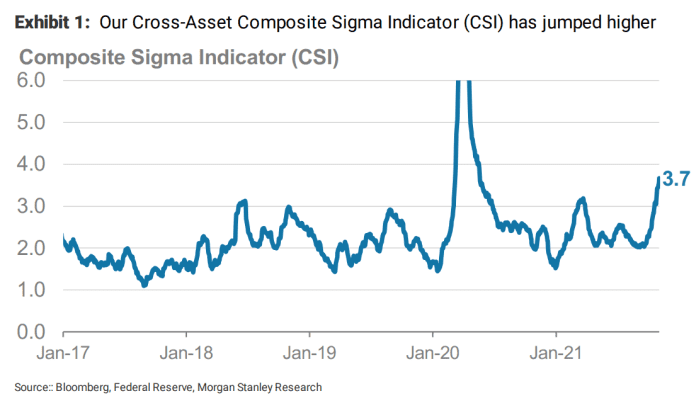

But below the surface, “volatility has jumped,” they wrote, unveiling a new cross-asset gauge, dubbed the Composite Sigma Indicator, which stands at its highest reading in five years with the exception of the COVID-induced turmoil of the second quarter of 2020 (see chart below). That reflects a rising number of extreme one-day moves, defined as a standard deviation of larger than 1.5.

Morgan Stanley Research

Anyone who has paid attention to the U.S. and global government bond markets in recent weeks probably won’t be surprised to learn that rates markets are at the heart of those moves. Indeed, the Composite Sigma Indicator has been driven by extreme moves in yield curves; inflation breakevens, which measure the difference between inflation-protected and nominal debt of the same maturity; and 2-year rates, the analysts said.

Short-term government bond yields, including those on 2-year U.S. Treasury notes

TMUBMUSD02Y,

began a sharp rise in September as investors began to pencil in a more aggressive stance by global central banks in response to inflation that has proven more persistent than expected. The gap between short- and long-dated yields narrowed significantly, a yield-curve phenomenon known as flattening.

The speed of the move has been interpreted by some investors as the potential harbinger of a “policy mistake,” in which central banks spark an economic downturn by tightening too aggressively. The moves also wrong-footed investors, leaving some high-profile hedge funds with large October losses, according to The Wall Street Journal.

Earlier: Hedge funds seen facing heavy losses amid wrong-way Treasury bets ahead of Fed tapering, traders say

Two-year rates in Poland, meanwhile, have risen by 85 basis points, or 0.85 percentage point, a 12.2 sigma deviation on the distribution of weekly moves for the rate, the analysts noted. The U.K. saw “extreme dislocations” as short-term rates rose and long-term rates fell, while in commodities markets, iron-ore prices are down 20%.

Related: Powell steers markets through Fed decision as international counterparts struggle

“Rates are the sole driver of this move, while other assets are unusually calm. Risk management in global rates feels very different from equities or FX heading into year-end,” the analysts wrote.

Stocks stumbled in September, but major indexes roared back in October and continue to press to all-time highs this month. The S&P 500

SPX,

was up 26.9% year to date through Friday, while the Dow Jones Industrial Average DJIA has rallied 21.2% and the Nasdaq Composite

COMP,

advanced 23.9%.

Read: ‘It’s a melt-up’: U.S. stocks are on an unusually strong run heading into the holidays

So what does it all mean? “It suggests that the liquidity environment is already shifting, even if not readily apparent in the S&P 500,” they said.

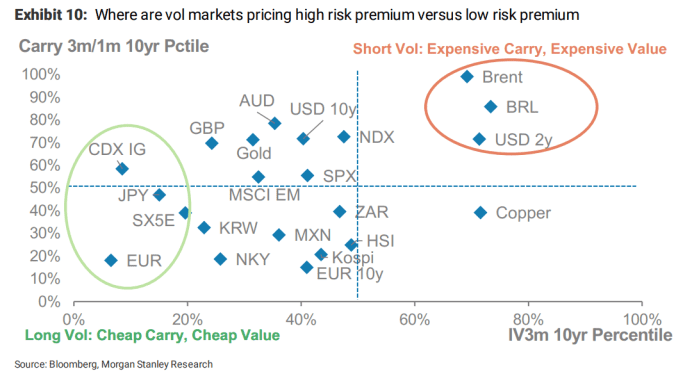

It also means that risk premium matters (see chart below).

Morgan Stanley Research

“Many of the markets with the largest recent moves were those priced for the calmest environments. As idiosyncratic risk rises, and risk management becomes more challenging, we see opportunities in high versus low risk premium markets,” they wrote.