This post was originally published on this site

Investors should buy Peloton Interactive Inc.’s stock, says Deutsche Bank analyst Chris Woronka, but only those who have the patience to ride out potential volatility, which could last a “few quarters.”

The at-home fitness company’s stock

PTON,

slumped 2.9% in midday trading, reversing an earlier intraday gain of as much as 4.6%.

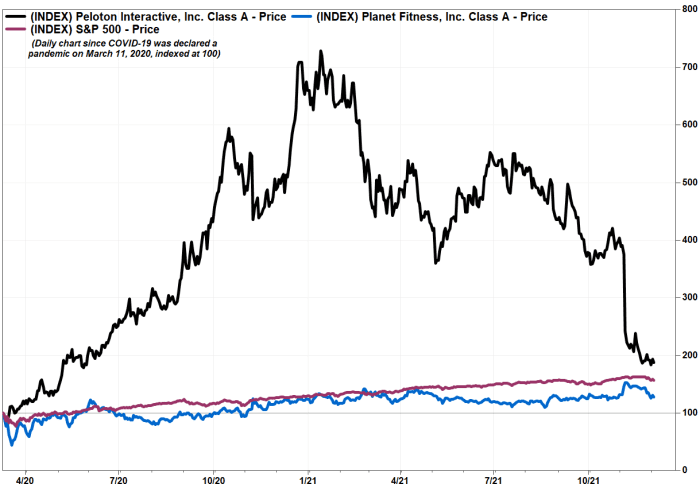

Peloton was viewed as a hot COVID-19-pandemic play last year, with the stock rocketing more than fivefold (up 434%), as gym closures fueled an explosion in the “work-in” trend. It’s been an entirely different play in 2021, however, as the stock has plunged 72% year to date, and closed Wednesday at $42.25, the lowest price since May 27, 2020.

In comparison, shares of fitness center operator Planet Fitness Inc.

PLNT,

have gained 3.6% this year and the S&P 500 index

SPX,

has rallied 21%.

Don’t miss: Peloton’s ‘stunning’ and ‘rapid deterioration’ of demand outlook prompts analysts to slash stock targets.

Also read: Peloton stock’s pain is the mirror opposite of Planet Fitness’ gain.

While the stock has suffered a “tough ride” this year, and the going could still be a bit rough for a while, Deutsche Bank’s Woronka said he is bullish on Peloton’s fundamentals over the longer term.

He initiated coverage of Peloton with a buy rating and a 12-month stock price target of $76, which implies nearly 80% upside from current levels. Woronka said his view is based on an “unemotional analysis” of the company’s earnings power in a “normalized, fully-reopened” economic environment.

“[W]hile it’s never fun to lead off a buy report with a ‘patience required’ asterisk of sorts, that’s exactly what we find ourselves doing here,” Woronka wrote in a note to clients.

As a fundamental analyst, Woronka said he is most interested in looking for “asymmetrical risk/reward scenarios,” and that’s what he believes Pelton’s stock provides at current levels. While there are scenarios in which the stock can still go lower, he believes there are more scenarios that result in even greater upside.

“Right now, we believe the market is looking at fitness stocks as an ‘either/or’ sector; either consumers stay at home to work out or they go back to their favorite pre-COVID-19 fitness facility,” Woronka wrote. “In our opinion, that’s an oversimplified view of the world; we think the hybrid work model extends to fitness, too, and that [Peloton] has plenty of momentum to regain operationally.”

FactSet, MarketWatch

He realizes that sentiment on the stock isn’t likely to reflect his bullish view “until a few quarters of improved execution” are in the books. But that’s where the opportunity for reward lies over a 12-month time horizon.

Once the stock starts trading on fundamentals again, Woronka believes “it has quite a bit of room to run.”