This post was originally published on this site

GE plans to split the conglomerate into three companies focused on aviation, healthcare and energy. We can’t know the ultimate outcome of such a split, but there is one absolute certainty: CEO Larry Culp will have extraordinary financial gains.

We know this is a certainty because Culp has an employment contract that guarantees it. It fits with how GE

GE,

has behaved for decades: executives have accumulated wealth regardless of how shareholders fared.

The most recent proxy statement filed with the SEC in March 2021 lists Culp’s total compensation for 2020 as $73,192,032, almost all from two stock awards. That includes a decision by the board in August 2020 to amend Culp’s contract to extend it and offer more performance shares at lower thresholds. Yes, some of the pay is not guaranteed because of vesting requirements. Such awards are theoretically designed to encourage long-term focus and are therefore considered “at risk,” particularly if the goals are rigorous, which they were not in this case.

Culp will be awarded between 4.6 million shares and 13.9 million shares, with vesting based on whether GE’s highest average closing price for any 30 consecutive trading days between Aug. 18, 2020 and Aug. 17, 2024 hits specific trading values, with a threshold, target and maximum payments.

However, the targets were set so low that GE’s stock price has already crossed the threshold that gives him the lowest number — not because of anything particular Culp had done but because GE’s stock price has generally tracked the bull market. If the stock maintains its current level for a few more weeks, Culp will be awarded the targeted number of shares. (He won’t officially get the shares until the end of his contract, which will also affect their ultimate value.)

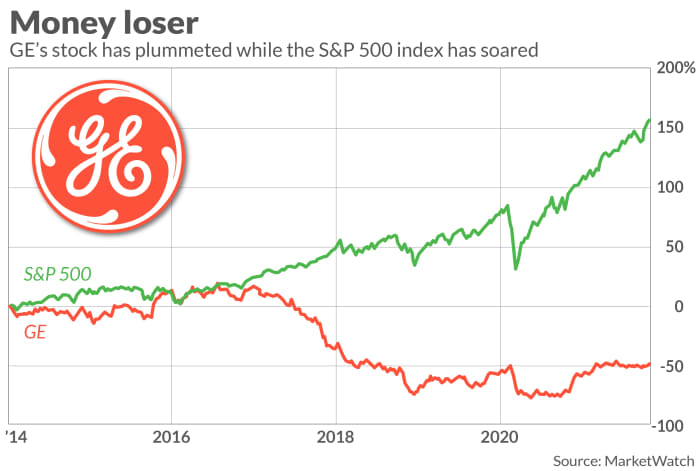

Most shareholders are far too lax on executive compensation, too often rubber-stamping pay packages. I know, because I spend my days looking at executive compensation packages as well as shareholder guidelines and voting practices. GE has made As You Sow’s of companies with overpaid CEOs in six out of the last seven years, beginning with the 2016 report that covers 2014 compensation. And GE’s stock has been a money-loser; from Jan. 1, 2014, when Jeffrey Immelt was still CEO, through Monday, before GE announced the plans for the three-way split, its stock plummeted 48 %. The S&P 500

SPX,

climbed 156%.

SOC Investment Group, which works with pension funds at four unions and was then known at CtW Group, argued in a letter ahead of the 2021 annual meeting that Culp’s award could be worth “a staggering $232.5 million at maximum. Astonishingly, the threshold performance hurdle is 12% lower than the stock price when Mr. Culp was hired” in October 2018.

More than 57% of GE shareholders voted against that pay package. Yet the vote is non-binding and came after the contract was signed. Will GE’s directors make more cautious compensation decisions going forward? We hope so, but that remains to be seen.

Now Culp could make even more. All companies are required to include in their proxy statements executives’ potential termination payments. Executives tend to get the biggest packages during change-in-control transactions, which can be either a sale or a spinoff. In its proxy statement the company estimated that if a change in control had taken place on Dec. 31, 2020, Culp’s performance awards would have been worth more than $100,389,802.

Whether GE’s plans to split into three companies will be a change in control may depend in part on whether “more than 50% of the surviving entity is controlled by the shareholders immediately prior to such event, in substantially the same proportions as their ownership immediately prior to the event.”

If it is considered a change in control, GE’s proxy statement explains that under Culp’s contract a variety of calculations will be made and the one that awards the CEO the highest payment –“the greatest of” according to the company — will be the one chosen. That “the greatest of” clause speaks volumes not just about GE but about the distorted values apparent in compensation.

Not only has GE provided excessive executive compensation to its CEOs, but its pay packages have helped fuel pay raises at other major companies. The use of peer benchmarking to pump up pay is a well-documented component of executive pay increase. Given the number of industries GE was in, many companies could and did list it as a peer comparison. Any company that did so had cover for increasing their own CEO’s pay.

Stock splits, buybacks, and spin-offs all affect a company’s stock price. The stock market responded favorably to GE’s latest plans. Shareholders who bought the stock at recent lows may be satisfied, and any shareholder is happy to see the price increase. But many institutional investors have likely held shares in their portfolio for many years. GE’s stock price was at its highest in August 2000, and at close on Tuesday was still just 25% of that price (after taking into account the 1-for-8 reverse split in August).

Executive compensation is a distorted system, and GE is just one example. Given all this, does Larry Culp deserve to receive such astonishing compensation [RLW6] for splitting up GE? To me and many other shareholders, the answer is no.

Rosanna Landis Weaver is the program manager for the wage justice and executive pay program at As You Sow, a nonprofit organization that promotes environmental and social corporate responsibility through shareholder advocacy.

More opinion: Why GE’s tax-free split could power the stock higher and reward patient investors