This post was originally published on this site

As the ravages of the latest COVID variant settle, stock markets are bracing for Yet Another Re-Opening trade (YARO).

Yes, here we go with the expert definition and nuances of the word “transitory” and the debate that follows as it applies to inflation. We have argued that the North Star in this current equity regime is an expansion of the profits cycle. The challenge in this period has become the start-stop-and-start-again motion of the re-opening as the complexities of COVID/supply chain events warp a traditional profits rebound.

We continue to make a case for investing in higher quality firms to better navigate this moment while limiting exposure to innovation firms to reduce risk. Secular highs in the valuation of innovation shares are a source of risk as interest rates reverse course and Fed-watching returns to prime time viewing.

Investors will shift their gaze again to a tapering tantrum. In this back and forth state of COVID-on, COVID-off, chasing the tails of the tape will leave investors tired as they frantically recalibrate their portfolios. The focus on higher quality with a valuation bias should offer the best path forward as investors weigh the chances of Yet Another Re-opening Trade.

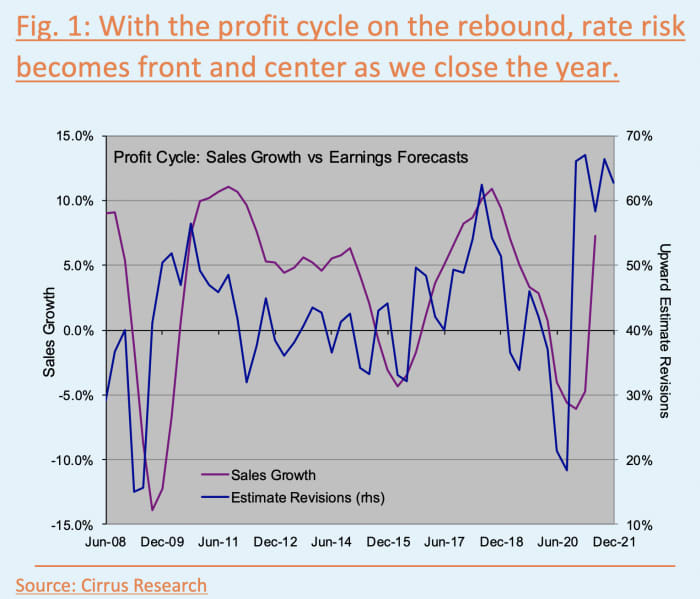

This see-saw action between weaker-than-expected inflation and liquidity-driven reflation fears has drained investors this cycle as we head into a likely choppy fourth quarter. As the global economy has started to reopen, albeit in a mixed fashion, sales growth in the U.S. has rebounded to a solid 7.4% year over year with the latest reporting.

In other words, the early stage gains are most likely behind us. Investors should position for continued expansion and look to firms with higher profit margin and better balance sheets .

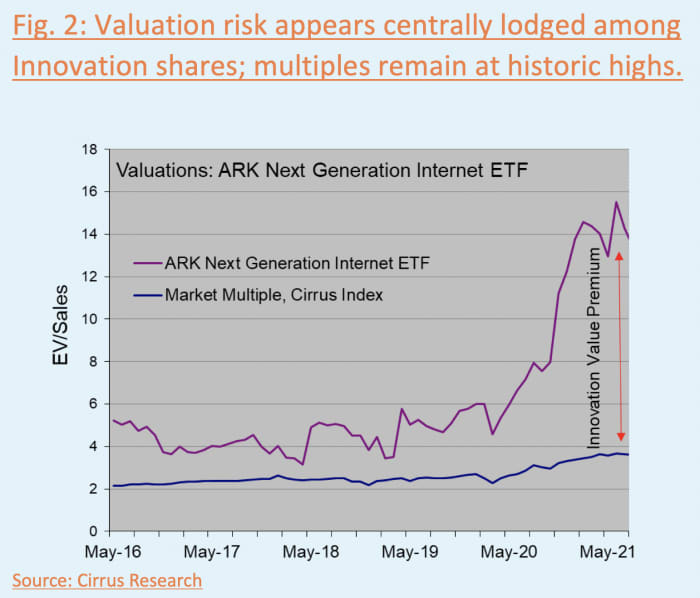

Importantly, high quality firms remain notably discounted as investors ignored basics such as margins and balance sheets to chase after liquidity-driven, innovation-centric names during the lock-down. This was further exacerbated as the vaccine/re-opening surge inflated deep cyclicals.

Combined, these elements explain why higher quality firms are selling at historical discounts. Relative to low quality, high-quality firms are trading at EV/Sales that are 1.4, 1.8, and 1.1 standard deviations below their historical averages for large-, mid- and small-cap firms, respectively.

The re-opening fallout should also continue to place upward pressure on rates, therefore adversely impacting aggressive growth, innovation shares.

COVID infection rates have begun to ebb, signaling a shift in markets from a narrow economy to a re-opening posture, again. To no surprise, Fed-watching has resurfaced as equities with rich multiples require low/favorable interest rate backdrop to thrive. A full-on re-opening of the global economy places aggressive growth firms trading at historic highs at risk.

We have seen rate risk for innovation baskets as they tumbled when rates rose in September. Historical data underscores another example of equity market performance sensitivity to interest rate swings. In a short span from the end of July to the end of September, yield on the 10-year Treasury note

TMUBMUSD10Y,

climbed to 1.46% from 1.18%. The equity-market fallout was quite direct — the Nasdaq Composite

COMP,

lost 1.53%, the growth index tumbled 1.10% and the technology sector shed 1.23%. Notice that as fears of the delta variant appear to be subsiding and vaccination rates began rising, investors’ focus has returned to re-opening and therefore central bank policy.

As U.S. businesses and schools reopen, the focus back to liquidity will continue to fuel the fears of nervous market participants struggling to weigh the durability of the Fed liquidity support. This nervousness temporarily faded as COVID variants attacked sizable regions within the states. If the jump in innovation stocks began with a historic surge in liquidity, investors are rightfully concerned that any attempt to taper the market support will have adverse spillover effects on the valuation of the most aggressive parts of the equity landscape.

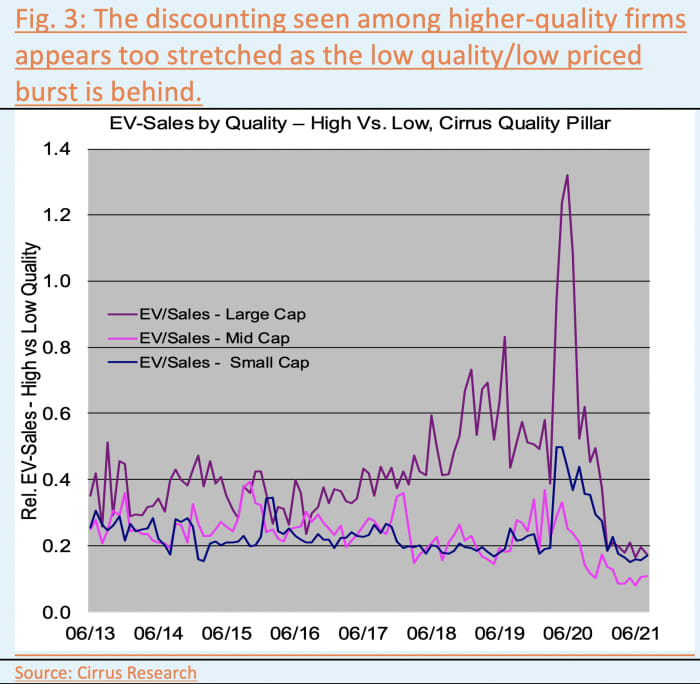

The innovation sector may be the epicenter of the market focus as interest rates become turbulent. Figure 2, below, demonstrates the high valuation of innovation firms as represented by the ARK Next Generation Internet ETF

ARKW,

At the end of August, the ARK Next Gen Internet ETF was trading at 13.4x EV/Sales vs. 3.6x EV/Sales for the large- and midcap markets.

More broadly, the technology sector is also trading at extremely rich levels. On a historical basis, the smaller-company technology sector is trading with a 85% premium to the broader market compared to long term 33% premium on a trailing EV/Sales basis. The large- and midcap technology sector is trading with a 113% premium to the broader market vs. the 58% historical premium.

Although shy of the peak multiples seen in February, smaller innovation stocks trade in excess of 20x sales and large-caps north of 19x sales. During the selloff in September, we witnessed large-cap innovation stocks weaken by more than 5%.

Bottom line: As the U.S. economy continues to re-open, it becomes clearer that the highest expectation firms cannot climb much higher or maintain the existing premia from current levels.

The North Star to the current environment remains an expanding profits cycle which will continue to force a valuation focus. Innovation firms will likely struggle as the re-opening takes hold and impacts interest rates adversely. Importantly, looking to firms with superior margins and better balance sheets will become more prominent as this recovering profit cycle ages.

Satya D. Pradhuman is CEO and director of research at Cirrus Research.

More: Big Tech stocks are the market’s superstars but rising rates could bring them down

Also read: These companies prove that when workers are happy, investors are too