This post was originally published on this site

For the first time since 2009, the 3-month U.S. Treasury bill rate is now higher than the yield on earnings derived from generally accepted accounting principles for companies in the S&P 500 Index.

That’s according to Ed Clissold, chief U.S. strategist, and Thanh Nguyen, senior quantitative analyst, at Ned Davis Research. In a note this week, they said rates on short-term T-bills have risen to levels that have prompted some investors to debate whether equities are worth the risk anymore, given the uncertainties that are keeping the S&P 500 Index

SPX,

from breaking above 4,200.

After a dismal year for both bonds and stocks in 2022, high-quality fixed income such as T-bills and investment-grade corporate bonds are having their moment — offering what investors see as better competitive returns. The Fed’s determination to restore price stability is pushing T-bill rates to multi-year highs, while putting a dent in the performance of most U.S. stocks in 2023, aside from the Nasdaq Composite Index

COMP,

which is up 20.9% for the year as of Friday.

The three-month T-bill rate remains near its highest level since January 2001, at 5.265%, according to 3 p.m. Eastern time data from Tradeweb. Meanwhile, 2-

TMUBMUSD02Y,

10-

TMUBMUSD10Y,

and 30-year Treasury yields

TMUBMUSD30Y,

all ended higher on Friday and advanced for the week.

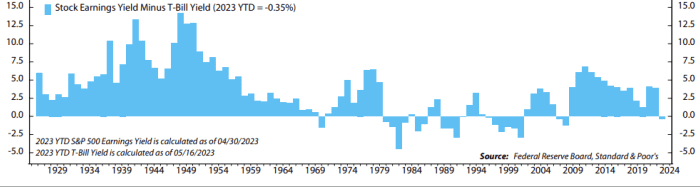

“After a decade of TINA (there is no alternative)” to equities, “markets have transitioned to TARA (there are reasonable alternatives),” Clissold and Nguyen wrote in their note. They cited the three month T-bill rate’s yield of more than 5.2% versus the S&P 500 GAAP earnings yield of 4.88% (see chart).

Source: Federal Reserve Board, Standard & Poor’s, Ned Davis Research

The S&P 500 has failed every attempt to break through the 4,200 level this year, and “the earnings outlook for 2023 does not appear to be strong enough by itself to save the market from competition from Treasury bills,” Clissold and Nguyen said.

Read: Buying stocks is just not worth the risk as equities are the most unattractive since 2007

A pause in debt-ceiling talks, along with the possible need for more mergers in the U.S. banking sector, sent all three major stock indexes to a lower finish on Friday.

Stocks were also weighed down on Friday by different interpretations of remarks made by Fed Chairman Jerome Powell. While Powell’s comments reinforced traders’ expectations for a pause by the Fed in June, some analysts described the Fed chairman as being a touch hawkish — leaving just enough room for policy makers to hike rates again if needed to control inflation.

For the year, the S&P 500 is up 9.2% and the Dow Jones Industrial Average DJIA is up only 0.8%, as of Friday.

Earlier this week, Mark Haefele, chief investment officer at UBS Global Wealth Management, said that “we see the risk-reward tradeoff for U.S. equities as unattractive.”

In a soft-landing scenario for the U.S. economy, UBS Global Wealth thinks the S&P 500 “could rise to 4,400 by year-end.” But if the economy slips into a recession, “we believe the market could fall to 3,300,” Haefele wrote in a note. “Given this asymmetric skew, we have a least preferred rating on equities relative to bonds, especially in an environment where high-quality fixed income offers competitive returns.”