This post was originally published on this site

Investors should have learned a valuable lesson in the past few weeks when it comes to IPOs.

If the valuation is sky-high, that may be something of a red flag, according to David Trainer, chief executive of independent equity research company New Constructs. The company uses machine learning and natural-language processing to parse corporate filings and model economic earnings, although its research has encountered pushback.

Chip maker Arm Holdings Ltd.

ARM,

and grocery-delivery app Instacart

CART,

both hit public markets at high valuations and both have fallen back since then, Trainer wrote in a new report.

The same may happen to Birkenstock Holding Ltd.

BIRK,

which is expected to debut next week. The German company known for its iconic sandals and clogs has plans to offer 32.3 million shares priced at $44 to $49 each.

The company would have a valuation of $8.7 billion at the midpoint of that price range, Trainer noted. That’s a bigger market cap than peers such as Skechers USA Inc.

SKX,

Crocs Inc.

CROX,

and Steve Madden Ltd.

SHOO,

For more, see: Birkenstock is going public: 5 things to know about the iconic German sandal maker’s IPO designs

“Even more shockingly, the only footwear companies with a larger market cap are Nike

NKE,

and Deckers Outdoor

DECK,

While Birkenstock is

profitable, we think it is fair to say that the $8.7 billion valuation mark is too high, especially for a company that was valued at just $4.3 billion in early 2021. Not a whole lot has changed since then,” the report said.

Trainer estimated that Birkenstock would need to generate more than $3.8 billion in annual revenue to justify that valuation, which is more than three times the $1.24 billion chalked up for all of 2022, according to its filing documents with the Securities and Exchange Commission.

“We don’t see this happening anytime soon, if ever,” the analyst said.

There are other issues, too. Birkenstock is planning to expand into global markets where it’s currently underrepresented, notably Asia Pacific. In fiscal 2022, the Americas made up 54% of its revenue, while Europe accounted for 36% and Asia Pacific just 10%.

But the company acknowledges in its F-1 filing that it faces “competition from counterfeit or ‘knockoff’ products,” due to the many countries that do not protect intellectual property (IP) rights to the same extent as the U.S.

U.S. companies have long complained and lobbied for greater IP protection in Asian countries, and in China, in particular.

Read now: Chinese IP theft is a ‘profoundly real challenge’ for U.S. economy, says Bridgewater’s McCormick

Counterfeits have been such a big factor in the past that Birkenstock took its products off the Amazon

AMZN,

marketplace, citing “unacceptable business practices which we believe jeopardize our brand.”

“While such a move certainly protects brand integrity, it also puts a cap on revenue growth potential — growth it will need to justify its IPO valuation,” said Trainer.

To be sure, Birkenstock has some things going for it, not least that it’s profitable and its customers are loyal, with 70% of existing U.S. consumers, for example, purchasing at least two pairs of its shoes, said Trainer.

A survey found 86% of recent purchasers said they wanted to buy again, while 40% said they did not even consider another brand while buying.

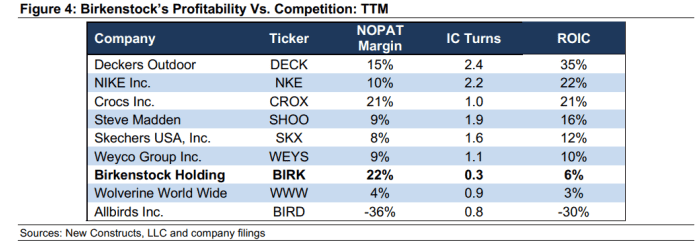

Still, the company has the lowest invested capital return among peers, a measure of balance sheet efficiency. As the following chart shows, Birkenstock’s return on invested capital is just 6%, below all but two of its peers, one of which is Allbirds

BIRD,

which Trainer has determined is one of his “Zombie Stocks,” or ones that he expects will fall to zero.

Source: New Constructs

And while 90% of its customers come through unpaid channels, the company’s costs are rising faster than its revenue, according to the F-1.

Selling and distribution costs rose 30% in the nine months through June 30 from the year earlier, while general and administration costs rose 50%, while revenue grew 21%.

“We don’t doubt that Birkenstock has strong brand equity and produces stylish sandals, but there is really no reason for this company to be public,” said Trainer. “We do not think investors should expect to make any money by buying this IPO.”

Trainer was also downbeat on Arm ahead of its IPO, warning investors that the company’s valuation was disconnected from fundamentals.

For more, read: Investors should avoid Arm IPO, New Constructs says

Arm’s stock was last trading just above $53, close to its issue price of $51. The stock closed up almost 25% above its issue price on its first day of trade but has languished since then.

Instacart, which trades as Maplebear, got similar treatment from Trainer, ahead of its IPO.

“The stock’s valuation implies the company will grow revenue by 24% each year for the next decade, a feat that is unlikely. CART looks more than fully valued, and we think investors should pass on this IPO. It’s okay for investors to be excited about the thawing IPO market, but that doesn’t mean they need to invest in every company that Wall Street offers to the public,” he wrote at the time.

Instacart was last trading just above $27, below its $30 issue price. That stock saw early gains of more than 40% in its debut but closed the first session up just 12%.

Read now: Instacart shares slump to their IPO price as investors have second thoughts

The Renaissance IPO ETF

IPO

has gained 25% in the year to date, while the S&P 500

SPX

has gained 11%.