This post was originally published on this site

Investors are eyeing companies for signs that inflationary pressures are eroding profitability, with more resilient businesses falling into favor in the stock market, according to Oxford Economics.

“This is an environment where pricing power and productivity growth is being increasingly rewarded,” said Daniel Grosvenor, director of equity strategy at Oxford Economics, in a report Thursday. “U.S. profit margins are likely to come under pressure in the near-term as costs continue to rise.”

Supply-chain disruptions and labor market shortages are driving up costs for companies, with many estimating that profit margins peaked during the second quarter, according to the report. Companies in the S&P 500 index

SPX,

may see a “modest decline” in those margins in the second half of 2021, weighing on U.S. stocks without derailing the bull market, Grosvenor wrote.

“Sectors and stocks with a proven track record of maintaining profit margins have started to outperform and this trend may continue in the near-term,” he said. Investors may continue to favor companies with “high pricing power and scope to grow and sustain productivity gains.”

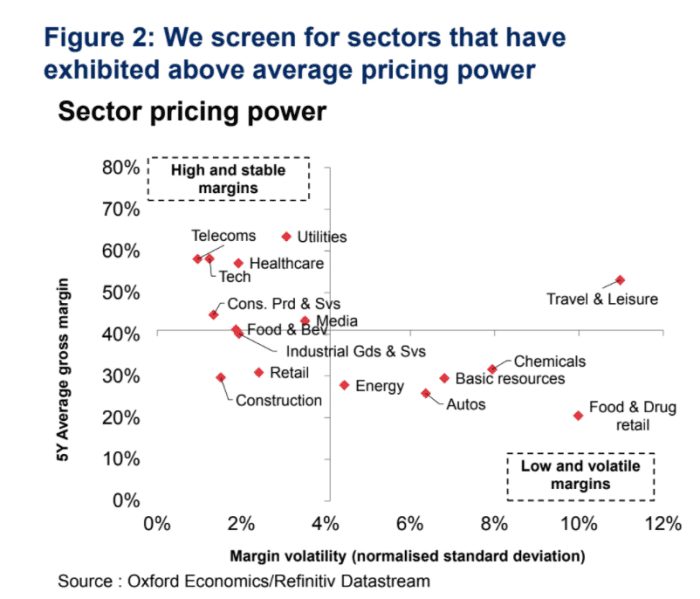

The Oxford Economics report shows that technology

XLK,

telecommunications

IYZ,

healthcare

IYH,

and the consumer products

IYK,

sectors are among the best positioned to maintain profit margins as the delta variant of the coronavirus continues to disrupt the economy in the pandemic. The “most vulnerable” sectors in the current environment include food and drug retail, chemicals and autos, said Grosvenor.

OXFORD ECONOMICS REPORT FROM SEPT. 16, 2021

The premium that investors are paying for shares of companies with high pricing power has increased significantly in recent months, expanding above pre-pandemic levels, according to the report. “This suggests that investors are already paying up for the greater certainty over earnings,” cautioned Grosvenor, “which is likely to limit any further gains.”

“If our base-case is correct that cost pressures ultimately prove transitory, then lower pricing power sectors and stocks may move back into favour as we head into 2022,” he wrote. That’s why Oxford Economics wouldn’t “indiscriminately” favor companies with high pricing power.

For example, “we are currently overweight healthcare as the sector appears relatively inexpensive, but we are underweight tech where valuations remain stretched versus historical norms,” said Grosvenor.