This post was originally published on this site

Here at MLPguy.com, I have never had a guest author or had a guest come on for an interview. Maybe 8-9 years ago, I almost had an MLP Tax expert come on to answer submitted reader questions, but he backed out citing compliance concerns (he was an attorney). I never tried again, until today.

Below is an interview with a guest that was conducted electronically with Will Hershey, an expert in the structuring of MLP-related ETFs, and he was eager to share his thoughts on the ALPS Advisors Alerian MLP ETF (NYSEARCA:AMLP) to help bring to light details of the fund’s structure that seem to be often overlooked by investors. Structural nuance of the vehicle is lost on many who seek simplified passive exposure to MLPs. We focused our discussion on AMLP, but the structural issues are not much different from other fund vehicles designed to own MLPs, including other ETFs and mutual funds structured as corporations.

I thought my readers would benefit from a thorough breakdown of the challenges of this ETF that is still used heavily by retail and institutional investors, despite its limitations.

Hinds: Will, we wanted to have you on because of your expertise in the structuring of exchange traded funds (ETFs), including your very relevant experience on the team that created multiple MLP-focused ETFs. Can you introduce yourself and your MLP ETF bonafides?

Will: Sure. I am the co-founder and CEO of Roundhill Investments, a registered investment adviser. I previously designed and helped to manage the Yorkville MLP High Income ETF and the Yorkville MLP High Income Infrastructure ETF, both of which were sold to a third-party in 2014. For more information on Roundhill Investments, readers can visit roundhillinvestments.com.

Hinds: Excellent. Now, the topic for our discussion is the most popular ETF that investors use to get broad exposure to MLPs. Can you give a brief overview of AMLP?

Will: The Alerian MLP ETF is the world’s most popular vehicle for investing in master limited partnerships. As of May 15, the fund had approximately $4.0 billion in AUM, representing nearly 3% of the total underlying market capitalization of the Alerian Infrastructure MLP Index (AMZI), the fund’s benchmark.

Aside from limited exposure to natural gas pipeline assets due to the limits of this vehicle owning exclusively MLPs, what are the main issues with the structure of the AMLP ETF?

While very popular, AMLP is also highly flawed from a structural standpoint. The 1940 Act fund structure prohibits funds from holding more than 25% of their holdings in limited partnerships. As a result, AMLP and other competing MLP-centric mutual funds, ETFs, and closed-end funds, are structured as C-corporations.

As C-corporations, these funds are potentially liable for a tax bill (as with any other corporation). Due to their potential tax bill, MLP fund auditors and tax consultants have determined that the optimal strategy to account for potential taxes due is to account for them in daily Net Asset Value (NAV).

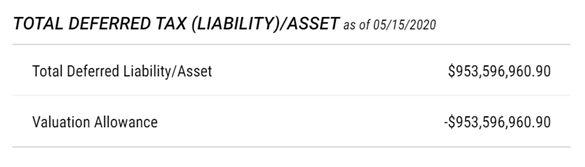

In practice, this means that these funds are required to set aside (i.e. extract from NAV) an amount equal to the potential taxes owed. In the case of these investment corporations, all potential tax owed is attributable to investments made, and therefore a combination of unrealized/realized gains (or losses). The unrealized portion of these gains (losses) is described by fund managers as a deferred tax liability (asset).

Source: ALPS

The thought behind this practice is relatively straightforward. As a corporation, the fund is liable for potential taxes due. If the fund were to close tomorrow (assume all investors redeem capital), the fund is on the hook to pay taxes on its profitable investments (as unrealized gains turn into realized gains). In order to treat all investors equitably, these potential tax payments are removed from Net Asset Value. (Imagine if they weren’t set aside and the fund closed the day after you invested, you would be unfairly paying a share of taxes due!).

Hinds: That’s the basic flaw that leads AMLP to underperform when MLPs trade up, as we’ve written about here (read our post on the subject here) and others have noted, correct?

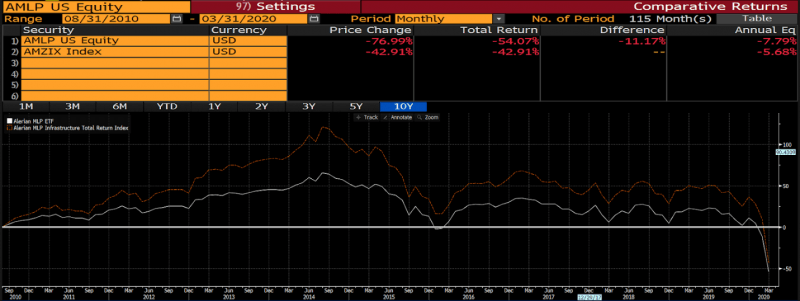

Will: Right. This information is well-documented, and many investors are aware of the resulting “tax drag”. In practice, this is borne out in fund returns that meaningfully lag that of their benchmarks – see below for AMLP.

Source: Bloomberg

In normal times (i.e. times at which the portfolio is carrying net unrealized gains), AMLP will appreciate roughly 77% that of the underlying benchmark. The remaining ~23% is set aside for potential taxes due. (For reference, this was previously closer to 65% and 35%, respectively. Favorable changes in capital gains taxes improved the structure in recent years).

Source: Global X

To illustrate, if the underlying index appreciates from 100 to 200, a newly launched MLP fund – tracking the same index – will appreciate from $100 to $177. Assuming the index drops back to 100, the fund will then decline back to $100, moving at a 0.77 delta to its underlying holdings.

However, when the underlying portfolio is carrying net unrealized losses, the fund will generally move lockstep with its underlying benchmark. This is due to what’s called a “valuation allowance”. While taxes being owed upon a full liquidation is a certainty, the potential benefits of utilizing unrealized losses is less clear. MLP fund accountants have therefore determined that a “valuation allowance” is required to offset the NAV improvement that would otherwise be afforded by allowing net unrealized losses to increase NAV.

To illustrate, if the underlying index depreciates from 100 to 50, a newly launched MLP fund – tracking the same index – will decline from $100 to $50. Assuming the index increases back to 100, the fund will then increase back to $100, moving at a 1.00 delta to its underlying holdings.

Hinds: That is all fascinating and very important for investors to understand. It doesn’t appear the market much cares for all that nuance, though, and the fund remains quite popular. Is there any other nuance that impacts the ability for this ETF to provide the exposure investors are seeking?

Will: Yes, actually. Things get even more tricky once we incorporate new inflows or outflows into the equation.

Let’s take the current case of AMLP. As outlined above, AMLP currently has a deferred tax asset of approximately $954 million. Due to the aforementioned “valuation allowance”, we would therefore expect AMLP to move at a delta of 1.00 relative to its underlying index until the point at which unrealized gains overwhelm unrealized losses.

Dividing the total deferred tax asset of $954 million by the shares outstanding (824,912,100) equals $1.16. If we add the $1.16 per share in deferred asset to the current NAV of $4.82, the result is $5.98. Therefore, we would expect the ETF to move at a 1.00 delta as it appreciates until $5.98, at which point any additional appreciation of $1 in the underlying holdings would translate into a $0.77 respective gain for the ETF. However, if the “low price” of the ETF and midstream more broadly, attracts material inflows, the potential upside can be further muted.

Let’s assume that retail investors pile into AMLP tomorrow. In total, a fresh $4.82 billion (solely used for simplicity reasons) is invested into the ETF. NAV remains unchanged. The total deferred tax asset, an absolute figure, remains unchanged. Shares outstanding, however, increased by 1 billion ($4.82 billion divided by NAV of $4.82). We now have 1 billion newly created shares in addition to 824,912,100 existing shares, for a total of 1,824,912,100. On a per share basis, the deferred tax asset has now been reduced from $1.16 to $0.52 ($953,597,961 divided by 1,824,912,100). As a result, the ETF will trade at a 1.00 delta on a rebound until only $5.34 ($4.82 + $0.52). Further appreciation in the underlying holdings will only amount to a $0.77 increase in NAV for every $1 appreciation in the underlying. The net result is a permanent impairment of upside potential.

Hinds: Wow, lots of details in there. But the detail you laid out was worth it. So, fund flows into the fund at a relative low point can skew your returns and limit the exposure investors are trying to get. Another reason to approach these very nuanced vehicles with caution.

Will: Agreed, and it’s frustrating to see it even as someone observing from a distance at this point. While I understand that investors may be attracted to its simple structure and lack of a K-1 that AMLP offers, be sure that you fully comprehend the potential risks. As investors pile in at bottom, like they did in April, it becomes increasingly difficult to achieve the previous levels, even if the underlying assets perform.

Hinds: Thank you for putting this information together and sharing it, Will, and also for being the first ever guest author on this site. Anything else you want readers to know before we finish up?

Will: Just a reminder that these answers have all been my opinions, and that I am not a tax advisor and nothing I said should be relied upon as investment or tax advice.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.