This post was originally published on this site

In a period of supply shortages, investors have an obvious play: Betting that commodity prices will continue to rise.

But shortages have also set up an opportunity in the futures market, with profits being made using the pricing curve indicated by futures contract prices.

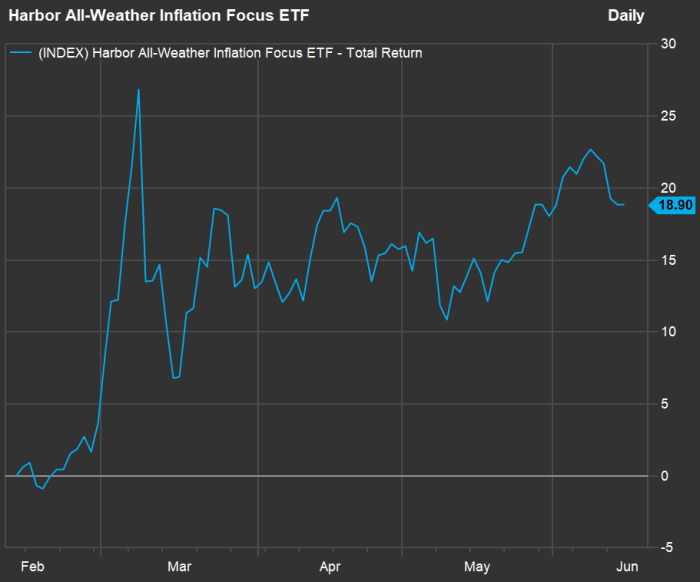

The opportunity is called “roll yield,” and it has enabled the Harbor All-Weather Inflation Focus ETF

HGER,

to perform well since it was established on Feb. 9, with a total return of nearly 19%:

FactSet

Harbor Capital Advisors has partnered with Quantix Commodities to manage HGER, which invests in futures across commodity classes.

During an interview, Spenser Lerner, the head of Multi Asset Solutions at Harbor Capital Advisors, said the current shortages of various commodities around the world might last for several years, as a similar shortage did in the 1970s.

Spot prices of commodities are high today, but futures prices going out three years are lower. This situation is known as backwardation.

It means that if a money manager maintains a portfolio of futures going out several years, profits can be made by selling futures contracts expiring in the near term, while purchasing contracts with maturities further out. Those profits are known as “roll yield.”

As of April 30, HGER’s roll yield was an annualized 27%. The roll yield for the portfolio is now still above 20%, Lerner said. (The opposite futures-market setup, in which commodity futures prices are higher in months and years ahead, is known as contango.)

Harbor Capital Advisors is based in Chicago and has about $55 billion in assets under management. Lerner and Jake Schurmeier manage about $1.5 billion through their asset allocation strategy.

Tailwind for oil

Lerner emphasized that HGER is diversified — it varies its focus across different types of commodities over time, putting more money to work on those for which the greatest roll yield is available. This makes it ideal for a time of high inflation.

Right now, the fund’s investments in oil futures make up about 46% of the portfolio. West Texas crude oil for July delivery

CL.1,

settled at $118.93 a barrel on June 14, up 61% from $75.21 at the end of 2021.

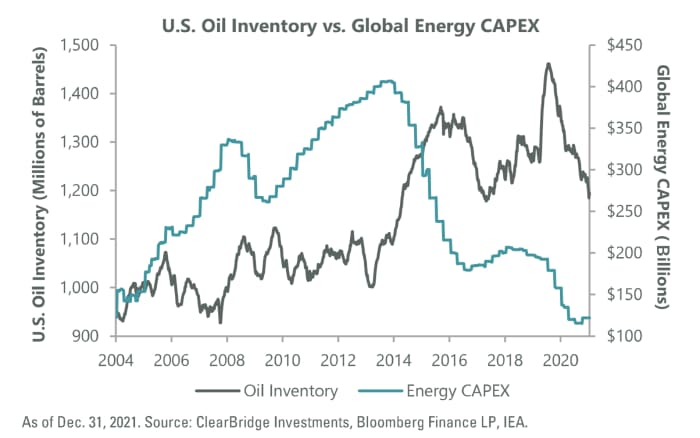

This chart shows that through the end of 2021, the stage was set for a long period of low supply for oil:

The chart was provided by Sam Peters, a portfolio manager at ClearBridge Investments, and most recently included this article about energy ETFs.

The left side of the chart shows that during previous economic cycles, oil industry capital expenditures increased when supplies were low. But the right side of the chart shows that in recent years, oil inventories and capital spending declined together. And comments from industry executives underscore how shy the industry is to make large investments in new supply.

During Chevron Corp.’s

CVX,

earnings call on April 29, CEO Michael Wirth emphasized budget discipline and said “one of the lessons in history is just as the bad times don’t last forever, neither do the times when prices are strong … we can’t start to believe that it will always be like this,” according to a transcript provided by FactSet.

During the same call, Chevron’s chief financial officer, Pierre Breber, said the company’s management team aims to “grow the enterprise at the lowest capital level.” He went further, saying: “There’s no time in our history where the market has valued growth and that’s why we emphasize return on capital,” which the company does through dividends and share buybacks.

Roll-yield strategy

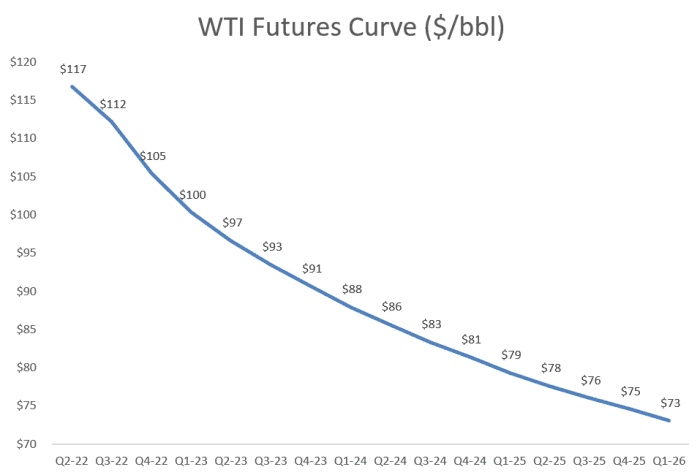

Lerner provided this chart, showing prices for West Texas Intermediate crude oil futures, going out to the first quarter of 2026:

Harbor Capital Advisors. Data source: Bloomberg.

Lerner was careful to point out that futures prices “aren’t great at actually telling you what prices will be.”

If oil prices were to shoot higher in the near term, the futures price curve would probably retain the same shape because of tight supply and the expectation that the supply/demand balance would shift over the long term.

Lerner said that in the opposite scenario — contango, with futures prices higher than spot prices — “you might prefer to own equities.”

He said the “roll yield can persist for a while,” and emphasized that shortages for commodities (excluding precious metals) are across the board. For example, “we have not seen the ramification” of the effect of Russia’s invasion of Ukraine on the wheat-planting season,” he said.

Even if oil prices were to fall significantly in the near term, the tight conditions for agricultural commodities might continue, Lerner said. One reason for this is that it takes time for refined fuel prices to decline after oil prices fall. High fuel prices have helped lead to higher prices for industrial metals, for example.

There’s no question that holding shares of energy companies this year has been a lucrative strategy, and those investments should perform well if oil prices hold, because the companies can continue raising dividends and repurchasing their shares, which lowers their share counts and raises earnings per share. The S&P 500 energy sector is the only of 11 sectors in the benchmark index to rise this year. It was up 50.6% this year through June 14, while the full index was down 21.6%.

The futures chart above shows investors expect oil prices to come down over the next few years. This is not to say that the oil companies would no longer be profitable. Simon Wong, an analyst at Gabelli Funds in New York, said during an interview in May that if WTI stays above $80, “these companies can still produce a lot of free cash that they can return to shareholders.”

But a price decline can take place even during an overall shortage. And that can cause a significant pullback in oil stock prices.

The roll-yield strategy is diversified and works in a high inflation environment. “You reduce the risk from any commodity falling,” Lerner said.

Don’t miss: Oil-stock trade is ‘too obvious,’ says this fund manager, who expects a pullback in prices