This post was originally published on this site

This week, we’ve identified another restaurant, providing a more home-style experience, positioned to survive the crisis and grow profits during the recovery. Cracker Barrel Old Country Store (CBRL) is this week’s Long Idea.

CBRL’s History of Profit Growth

We first featured CBRL as a Long Idea in March 2017 and closed the position in June 2018. CBRL was recently featured in our June 2019 article “3 Undervalued Stocks in the Restaurant Industry.” Now, with CBRL down 34% year-to-date (YTD), it trades at its cheapest valuation in years, as measured by price-to-economic book value (PEBV). For investors willing to look past the current crisis, CBRL represents a great buying opportunity.

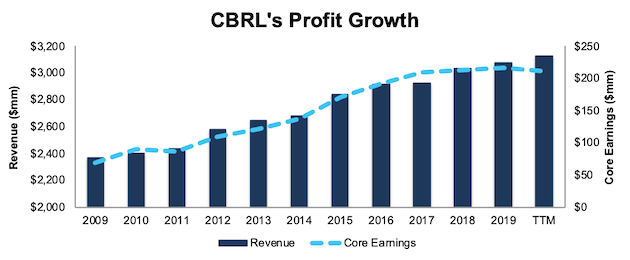

Prior to the COVID-19 outbreak, CBRL had a strong history of profit growth. Over the past decade, CBRL grew revenue by 3% compounded annually and core earnings[1] by 12% compounded annually, per Figure 1. The firm increased its core earnings margin year-over-year (YoY) in eight of the past ten years, and its core earnings margin of 7% over the trailing-twelve-months is up from 4% in 2010.

Figure 1: CBRL Core Earnings & Revenue Growth Since 2009

Sources: New Constructs, LLC and company filings

CBRL’s rising profitability helps the business generate significant free cash flow (FCF). The company generated positive FCF in each of the past 10 years and a cumulative $1.1 billion (47% of market cap) over the past five years. CBRL’s $145 million in FCF over the TTM period equates to a 4% FCF yield, which is significantly higher than the Consumer Cyclicals sector average of 1%.

Executive Compensation Plan Incentivizes Prudent Capital Stewardship

No matter the macro environment, investors should look for companies with executive compensation plans that directly align executives’ interests with shareholders’ interests.

Quality corporate governance incentivizes executives to create shareholder value, and they are held accountable for capital stewardship.

In fiscal 2019, performance shares made up 50% of CBRL’s long-term incentive program. These performance shares are tied to the company’s return on invested capital (ROIC). CBRL has included ROIC as a performance metric in its executive compensation plan since 2011, over which time CBRL has improved ROIC from 9% in 2011 to 14% TTM. The focus on improving ROIC aligns the interests of executives and shareholders and helps to ensure quality capital allocation.

Cracker Barrel’s Balance Sheet Provides Ample Liquidity to Survive the Crisis

Companies with strong cash flows and minimal debt are better positioned to survive macro-economic uncertainty. To conserve liquidity and ensure it has the cash to survive the current disruptions to operations, CBRL has suspended its dividend and share purchase activity. The firm also recently announced that it borrowed the remaining available amount under its Revolving Credit Facility, which gives the firm ~$400 million in cash available for ongoing operating needs.

In CBRL’s latest quarterly filing, the firm spent $210 million on store operating and general and administrative expenses. In a worst-case scenario, where CBRL is forced to close all its stores, furlough/lay off workers, and generates no revenue, its current cash could cover these expenses for nearly six months before needing additional capital. It is very unlikely that CBRL’s revenue would go to zero since the firm is currently providing to-go and delivery options and selling retail goods through its e-commerce store.

Furthermore, CBRL is heavily concentrated in states that have already announced, or are actively seeking dates, to reopen dine-in restaurant capacity. Based on these announcements, 28%-43% of CBRL’s restaurants could be open for dine-in service in May.

Superior Profitability to Survive and Expand During Recovery

Before the current crisis, Cracker Barrel’s profitability was trending higher at a faster pace than the full-service restaurant peers under coverage. Peers in the analysis below include Bloomin’ Brands (BLMN), The Cheesecake Factory (CAKE), Brinker International (EAT), Darden Restaurants (DRI), and more.

This superior profitability is a testament to CBRL’s hybrid restaurant/retail business model. High profitability also provides CBRL with greater resources to survive the current downturn and to gain market share when the economy rebounds.

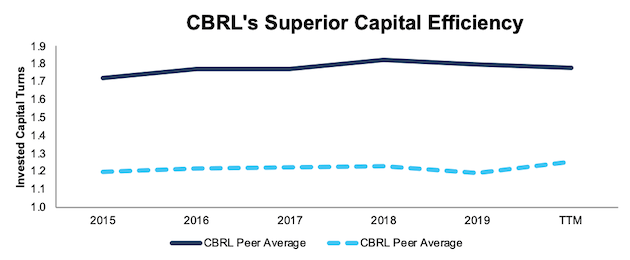

Per Figure 2, CBRL’s capital efficiency is well above peers’, as it has improved its invested capital turns from 1.7 in 2015 to 1.8 TTM. The market-cap-weighted average invested capital turns of peers improved from 1.2 to 1.3 over the same time.

Figure 2: CBRL’s Invested Capital Turns Vs. Peers

Sources: New Constructs, LLC and company filings.

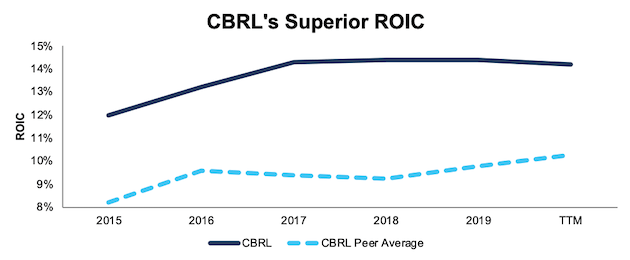

CBRL’s operational efficiency, or net operating profit after-tax (NOPAT) margin, while below the market-cap-weighted average of peers, has improved from 7.0% in 2015 to 8.0% TTM. The peer average has improved from 7.8% to 8.5% over the same time.

The combination of rising margins and invested capital turns drives CBRL’s ROIC higher. CBRL has improved its ROIC from 12% in 2015 to 14% TTM. Per Figure 3, the market-cap-weighted average ROIC of peers has increased from 8% to 10% over the same time.

Figure 3: CBRL’s ROIC vs. Peers

Sources: New Constructs, LLC and company filings.

CBRL’s superior profitability shows that its investment in operational efficiency, supply chain management, and retail inventory management gives it a competitive advantage. Moving forward, CBRL’s higher profitability allows the firm significant flexibility to adapt to decreased demand in store, focus on to-go orders, and ramp up operations when consumers can eat out once again.

Bear Case Assumes Restaurant Industry Never Recovers

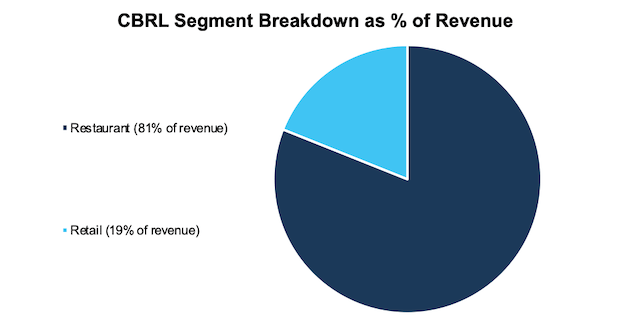

There’s no denying that the COVID-19 pandemic, has, and will, permanently alter the overall restaurant industry. With nearly 700 company-owned restaurants (as of January 31, 2020), most of which operate a restaurant and retail store (see Figure 4 for revenue breakdown), CBRL will certainly see decreased revenue and profits in the short term.

However, CBRL’s current valuation implies that (1) CBRL won’t generate any revenue during the pandemic and (2) the current crisis is not temporary, but forces a permanent decline in economic activity.

Figure 4: CBRL Restaurant vs. Retail Revenue Breakdown – TTM

Sources: New Constructs, LLC and company filings

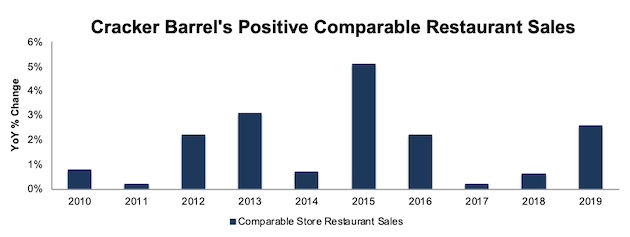

To buy into the current valuation, one must ignore the strength of Cracker Barrel’s brand and the firm’s ability to attract consumer dollars. Per Figure 5, CBRL’s comparable store restaurant sales have grown YoY for 10 consecutive years and accelerated over the last three years. Over this same time, comparable store retail sales have grown YoY in every year except 2010, 2017, and 2018.

Undoubtedly, we expect comparable store sales to decline sharply in the short term, but we, along with the International Monetary Fund (IMF) and nearly every economist in the world, believe that U.S. GDP growth will be higher in 2021 than expected before the pandemic. Accordingly, it is safe to assume the restaurant business will return to something, at a minimum, approaching historical levels. In such an event, Cracker Barrel is well-positioned to capitalize on the long-term demand to eat out, continue to grow profits, and take the market share left by the restaurants that do not survive the crisis.

Figure 5: Cracker Barrel Growing Comparable Store Restaurant and Retail Sales

Sources: New Constructs, LLC and company filings

Revenue Growth Despite Shutdowns: Growing “Off-Premise” Business

Restaurants that can offer to-go and delivery (collectively “off-premise”) service while customers are unable to eat in store can generate more revenue than those that do not.

Prior to the crisis, Cracker Barrel made key investments in its off-premise operations. In fiscal 1Q20 (period ended November 1, 2019), Cracker Barrel expanded its third-party delivery coverage to include nearly 600 stores (up from 350 in fiscal 3Q19). More recently, on April 27, 2020, Cracker Barrel announced a partnership with food delivery provider DoorDash that will allow customers to get discounts on Cracker Barrel’s “Family Meal Baskets To-Go.”

Most importantly, Cracker Barrel is growing its off-premise operations as demand grows for these options. In fiscal 2019, off-premise sales accounted for 9% of CBRL’s total revenue. In fiscal 2Q20 (period ended January 31, 2020), off-premise sales already accounted for 13% of CBRL’s revenue.

These operations help build deeper customer relationships and increase the ways in which consumers can enjoy Cracker Barrel food. In addition, off-premise orders generate a significant revenue stream to help the firm survive the crisis.

Market Share for the Taking After COVID-19

The stark reality is many smaller restaurants will not survive the current crisis. A study in late March conducted by the National Restaurant Association found that 11% of restaurant owners and operators anticipated they would permanently close within the next 30 days. CBRL’s financial position, along with its strong brand, position it to gain market share once the economy reopens.

CBRL Trades at Cheapest Level in Years

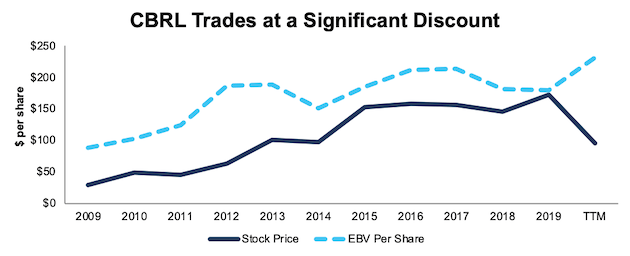

After falling 34% YTD, CBRL now trades at its cheapest PEBV ratio (0.4) since 2012. This ratio means the market expects CBRL’s NOPAT to permanently decline by 60%. This expectation seems overly pessimistic over the long term. For reference, during the Great Recession, CBRL’s NOPAT fell 4% YoY in 2008 before growing 4% and 17% YoY in 2009 and 2010.

CBRL’s current economic book value, or no-growth value, is $232/share – a 127% upside to the current price.

Figure 6: CBRL’s Stock Price vs. Economic Book Value (EBV)

Sources: New Constructs, LLC and company filings.

CBRL’s Current Price Implies Worst-Case Scenario

Below, we use our reverse DCF model to quantify the cash flow expectations baked into CBRL’s current stock price. Then, we analyze the implied value of the stock based on different assumptions about COVID-19’s impact on the restaurant industry and CBRL’s future growth in cash flows.

Scenario 1: Using industry projections, CBRL’s current revenue, and its historical margins, we can model the worst-case scenario already implied by CBRL’s current stock price. In this scenario, we assume the following:

- NOPAT margins permanently fall to 4.9% – which equals the firm’s lowest margin from 2007-2010, compared to 8.0% TTM

- Revenues fall 27% in 2020 – which is the worst-case scenario for restaurant sales proposed by Technomic, a food service industry research provider – and don’t grow again for two more years

- Sales begin growing again in 2023, but only at 3% a year, which equals CBRL’s revenue CAGR over the past decade

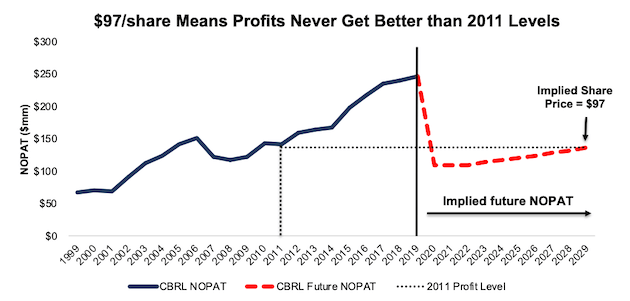

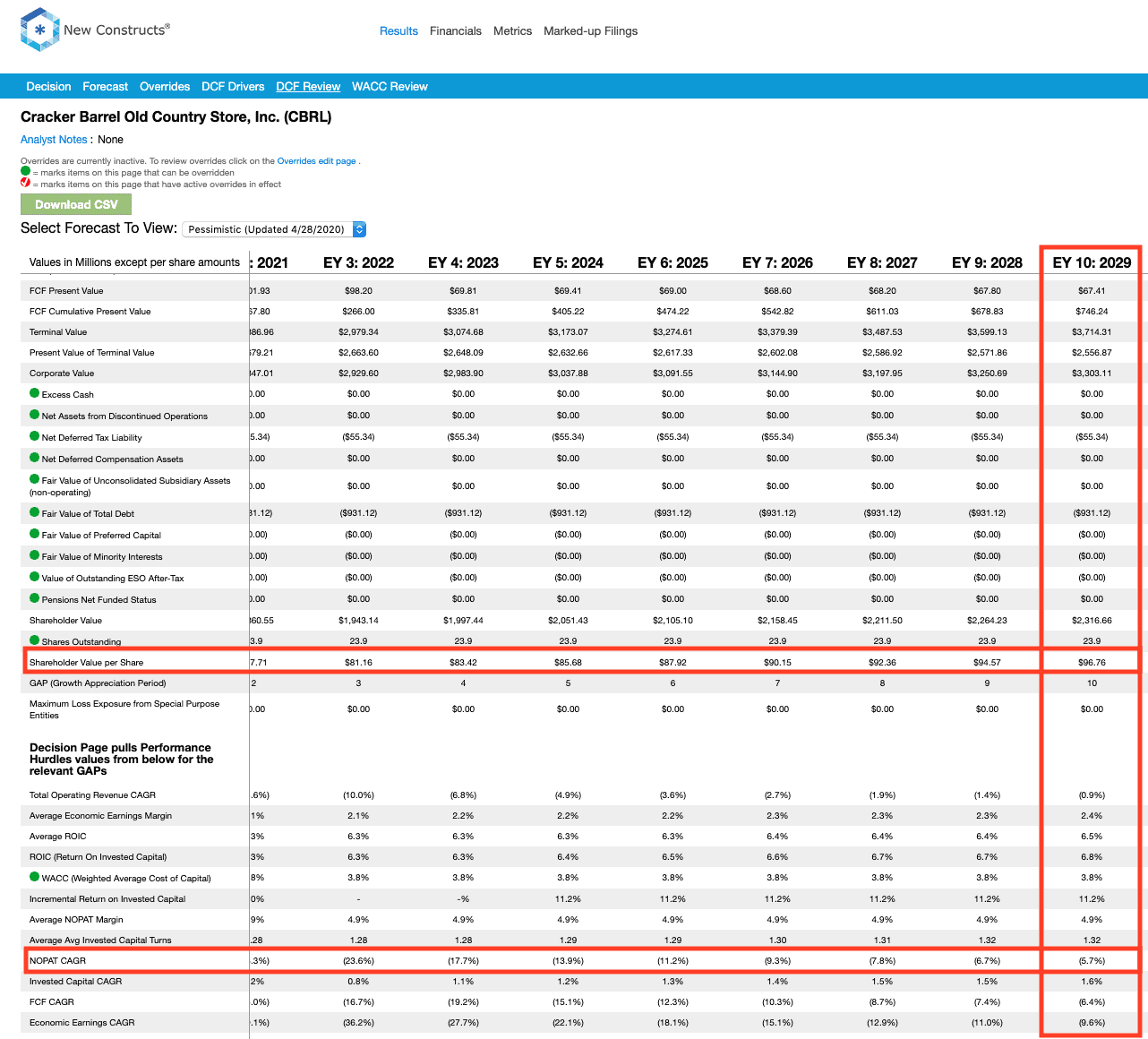

In this scenario, where CBRL’s NOPAT declines 56% in 2020 and 6% compounded annually over the next decade, the stock is worth $97/share today – equal to the current stock price at the time of writing. See the math behind this reverse DCF scenario.

Figure 7 compares the stock’s implied future NOPAT to the firm’s historical NOPAT in this scenario. This worst-case scenario implies CBRL’s NOPAT 10 years from now will be 44% below its 2019 NOPAT. In other words, this scenario means that a decade after the COVID-19 pandemic, Cracker Barrel’s profits will have only recovered to around 2011 levels. In any scenario better than this one, CBRL holds significant upside potential, as we’ll show below.

Figure 7: Current Valuation Implies Severe, Long-Term Decline in Profits: Scenario 1

Sources: New Constructs, LLC and company filings.

Scenario 2: Cheap Valuation Provides Significant Upside

If we assume, as does the International Monetary Fund (IMF) and nearly every economist in the world, that the global economy grows strongly in 2021, CBRL looks even more undervalued.

In this scenario, we assume:

- NOPAT margins fall to 4.9% in 2020 (company low from 2007 to 2010) before returning to CBRLs 5-year average NOPAT margin of 7.7% in 2021

- Revenues fall 17% in 2020, which is the mid-case scenario for restaurant sales outlined by Technomic

- Sales growth returns in 2021 at the IMF’s global base-case GDP growth rate of 5.8%

- Sales continue to grow at 3% a year, equal to CBRL’s revenue CAGR over the past decade, each year thereafter

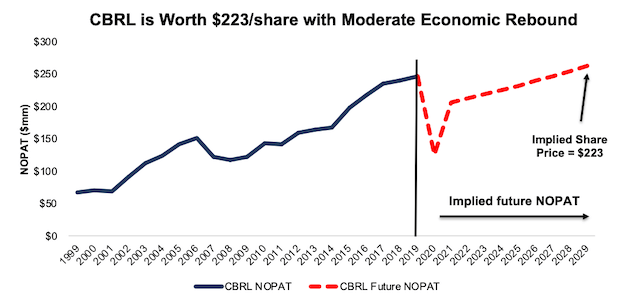

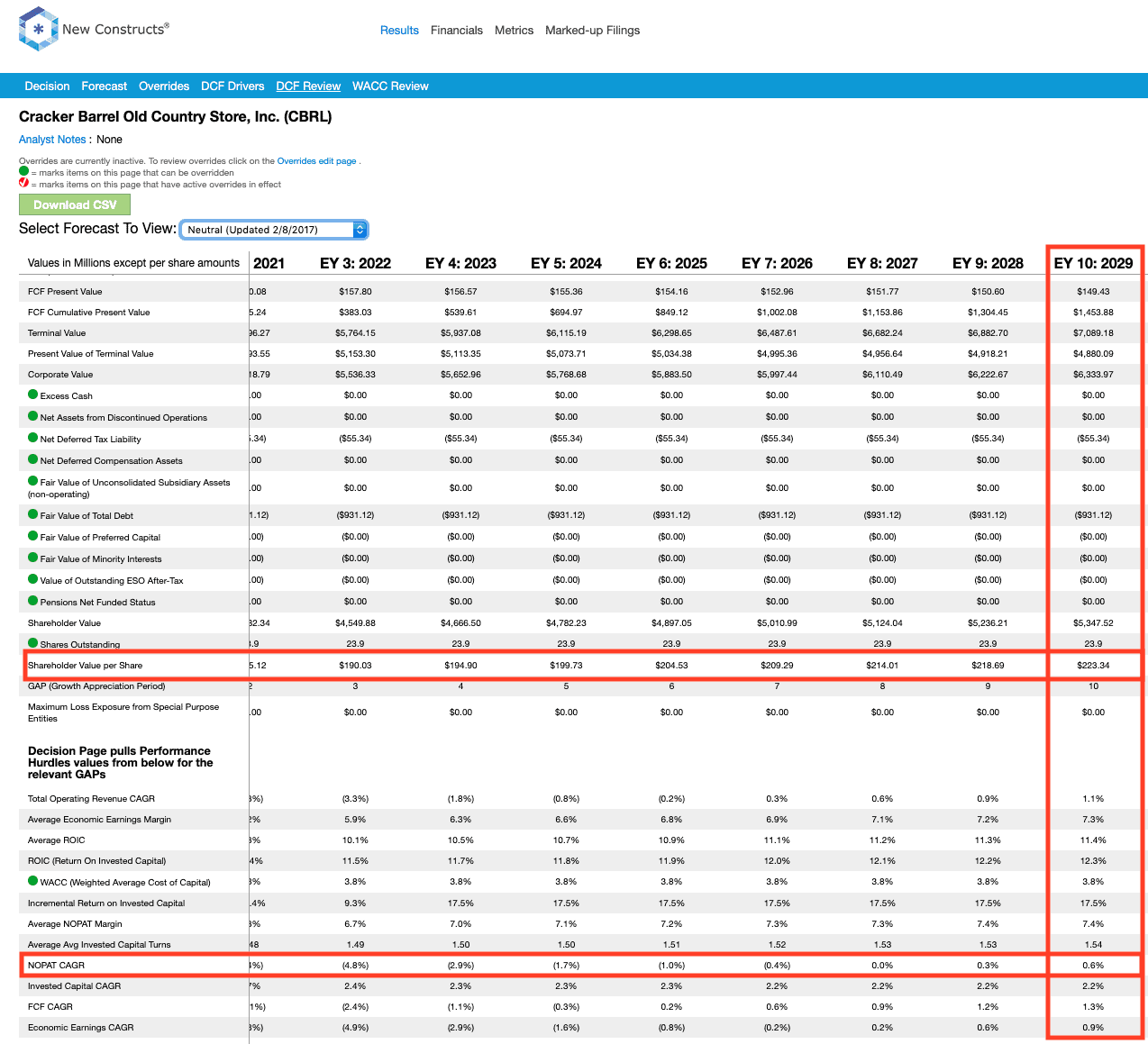

In this scenario, CBRL’s NOPAT falls 49% in 2020 and grows by just 1% compounded annually over the next decade, and the stock is worth $223/share today – a 119% upside to the current price. See the math behind this reverse DCF scenario.

It’s not often investors get the opportunity to buy a leading firm at such a discounted price.

Figure 8 compares the stock’s implied future NOPAT to the firm’s historical NOPAT in scenario 2.

Figure 8: Implied Profits Assuming Global Recovery in 2021: Scenario 2

Sources: New Constructs, LLC and company filings.

Sustainable Competitive Advantages Will Drive Shareholder Value Creation

Here’s a summary of why we think the moat around CBRL’s business will enable it to continue to generate higher NOPAT than the current market valuation implies. The following competitive advantages help CBRL profitability serve customers and prevent competition from taking market share:

- Higher profitability than peers

- Hybrid restaurant & retail stores across 45 states

- Liquidity to survive downturn

- Growing off-premise business helps weather the storm and provides long-term growth opportunities

What Noise Traders Miss with CBRL

These days, fewer investors focus on finding quality capital allocators with shareholder-friendly corporate governance. Instead, due to the proliferation of noise traders, the focus is on short-term technical trading trends while high-quality fundamental research is overlooked. Here’s a quick summary of what noise traders are missing:

- Core earnings growth and free cash flow generation over the past decade

- Cracker Barrel’s ability to consistently grow comparable store sales over the past decade

- Industry leader in a position to excel after the global pandemic subsides

- Valuation implies the economy never fully recovers from COVID-19

Suspended Dividend Should Be Temporary

As noted above, CBRL management recently suspended its quarterly dividend and share repurchase program to maintain flexibility and liquidity during the current economic downturn. Prior to this suspension, CBRL’s standard quarterly dividend provided a 5.4% yield, and the firm had increased its dividend in each of the last 10 years. We expect the current suspension to be temporary, and for CBRL to return capital to shareholders through dividends again after the economy rebounds.

In the past five years, CBRL has generated more free cash flow than it has paid out in dividends. CBRL generated a cumulative FCF of $1.1 billion over the past five years and paid out $949 million in dividends over the same time. FCF exceeded dividend payments by an average of $24 million per year over this time.

Firms with cash flows greater than dividend payments have a higher likelihood to maintain and grow dividends. While CBRL suspended its dividend in the short term, investors buying at current prices should get a nice yield with upside potential as CBRL reinstates the dividend over the long term.

In addition to dividends, CBRL has occasionally returned capital to shareholders through share repurchases. Through the first six months of fiscal 2020, CBRL repurchased $20 million worth of shares. The firm did not repurchase any shares in fiscal 2019. CBRL was authorized to repurchase an additional $25 million worth of shares prior to the suspension. Should the firm resume share repurchases once the crisis is over, the yield for investors will only increase.

An Earnings Beat of Depressed Expectations Could Send Shares Higher

According to Zacks, consensus estimates at the end of January pegged CBRL’s 2020 earnings at $9.11/share. Jump forward to April 27, and consensus estimates for CBRL’s 2020 earnings have fallen to just $2.65/share.

While the short-term impact of the COVID-19 pandemic is yet to be seen, these lowered expectations provide a great opportunity for a high-quality business, such as CBRL, to beat expectations over the long term. Though our current Earnings Distortion Score, which is a short-term indicator of the likelihood to beat or miss expectations, for CBRL is “Miss”, lowered expectations moving forward could make it much easier to beat earnings.

Additionally, the most obvious concern for CBRL in the short term is the numerous stay-at-home orders and inability to serve customers in store. However, as states across the country ease restrictions and consumers return to restaurants, positive signs of increasing demand could send shares higher.

Insider Trading and Short Interest Trends

Over the past three months, insiders have purchased a total of three thousand shares and sold no shares for a net effect of three thousand shares purchased. These purchases represent less than 1% of shares outstanding.

There are currently 2.3 million shares sold short, which equates to 10% of shares outstanding and three days to cover. Short interest is up 5% from the prior month, which indicates investors are too focused on the dip and not the recovery afterwards.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings as shown in the Harvard Business School and MIT Sloan paper, “Core Earnings: New Data and Evidence”.

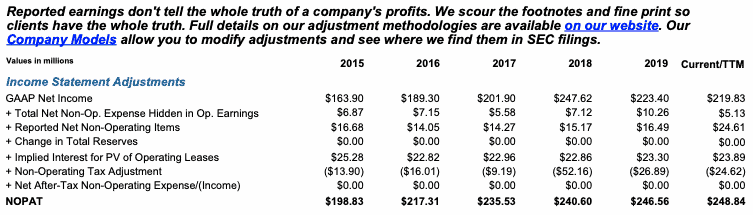

Below are specifics on the adjustments we make based on Robo-Analyst findings in Cracker Barrel Old Country Store’s 2019 10-K:

Income Statement: we made $77 million of adjustments with a net effect of removing $23 million in non-operating expenses (1% of revenue). See all adjustments made to CBRL’s income statement here.

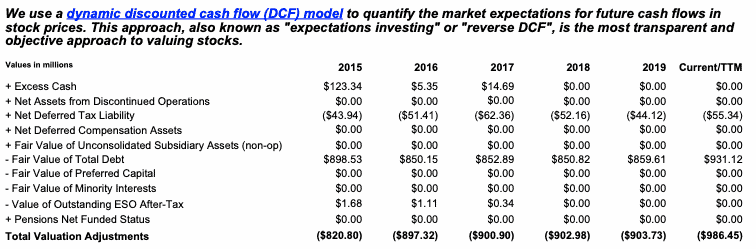

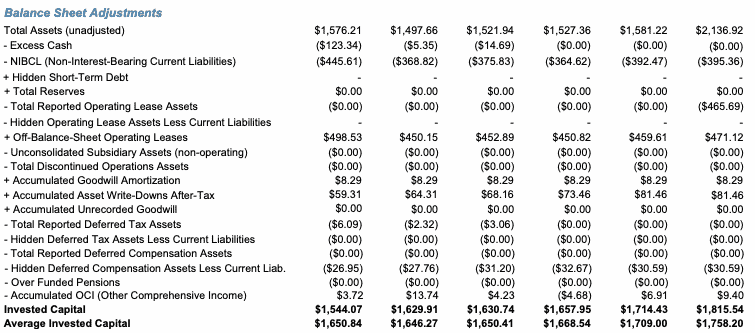

Balance Sheet: we made $615 million of adjustments to calculate invested capital with a net increase of $497 million. One of the most notable adjustments was $460 million (39% of reported net assets) in operating leases. See all adjustments to CBRL’s balance sheet here.

Valuation: we made $986 million of adjustments with a net effect of decreasing shareholder value by $986 million. There were no adjustments that increased shareholder value. Apart from total debt, which includes the operating leases noted above, the most notable adjustment to shareholder value was $55 million in deferred tax liabilities. This adjustment represents 2% of CBRL’s market cap. See all adjustments to CBRL’s valuation here.

Attractive Funds That Hold CBRL

The following funds receive our Attractive-or-better rating and allocate significantly to Cracker Barrel.

- ICON Equity Income Fund (IOECX) –3.0% allocation and Very Attractive rating.

- Second Nature Thematic Growth Fund (CEGYX) – 2.8% allocation and Very Attractive rating.

- Ivy Mid Cap Income Opportunities Fund (IVOCX) – 2.8% allocation and Attractive rating.

- Federated Global Strategic Value Dividend Fund (GVDIX) – 2.0% allocation and Very Attractive rating.

This article originally published on April 29, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

[1] Our core earnings are a superior measure of profits, as demonstrated in In Core Earnings: New Data & Evidence a paper by professors at Harvard Business School (HBS) & MIT Sloan. The paper empirically shows that our data is superior to “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).

Get our long and short/warning ideas. Access to top accounting and finance experts.

Deliverables:

1. Daily – long & short idea updates, forensic accounting insights, chat

2. Weekly – exclusive access to in-depth long & short ideas

3. Monthly – 40 large, 40 small cap ideas from the Most Attractive & Most Dangerous Stocks Model Portfolios

See the difference that real diligence makes.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}